Fit a linear mixed model via penalized maximum likelihood.

Usage

plmm(

design,

y = NULL,

K = NULL,

eta = NULL,

penalty = "lasso",

init = NULL,

gamma,

alpha = 1,

lambda_min,

nlambda = 100,

lambda,

eps = 1e-04,

max_iter = 10000,

dfmax = NULL,

warn = TRUE,

trace = FALSE,

save_rds = NULL,

return_fit = TRUE,

...

)Arguments

- design

The first argument must be one of three things: (1)

plmm_designobject (as created bycreate_design()) (2) a string with the file path to a design object (the file path must end in.rds) (3) amatrixordata.frameobject representing the design matrix of interest.- y

Optional: In the case where

designis amatrixordata.frame, the user must also supply a numeric outcome vector as theyargument. In this case,designandywill be passed internally tocreate_design(X = design, y = y).- K

Similarity matrix used to rotate the data. This should either be: (1) a known matrix that reflects the covariance of y, (2) an estimate (Default is \(\frac{1}{p}(XX^T)\)), or (3) a list with components

sandU, as returned by a previousplmm()model fit on the same data.

Note: If a user provides their ownKmatrix, it is decomposed as provided and will not be scaled. User-provided K functionality is currently not supported for filebacked data.- eta

Optional argument to input a specific eta term rather than estimate it from the data. If K is a known covariance matrix that is full rank, this should be 1.

- penalty

The penalty to be applied to the model. Either "lasso" (the default), "SCAD", or "MCP".

- init

Initial values for coefficients. Default is 0 for all columns of X.

- gamma

The tuning parameter of the MCP/SCAD penalty (see details). Default is 3 for MCP and 3.7 for SCAD.

- alpha

Tuning parameter for the Mnet estimator which controls the relative contributions from the MCP/SCAD penalty and the ridge, or L2 penalty.

alpha = 1is equivalent to MCP/SCAD penalty, whilealpha = 0would be equivalent to ridge regression. However,alpha = 0is not supported; alpha may be arbitrarily small, but not exactly 0.- lambda_min

The smallest value for lambda, as a fraction of the maximum lambda. Default is .001 if the number of observations is larger than the number of covariates and .05 otherwise.

- nlambda

Length of the sequence of lambda. Default is 100.

- lambda

A user-specified sequence of lambda values. By default, a sequence of values of length

nlambdais computed, equally spaced on the log scale.- eps

Convergence threshold. The algorithm iterates until the RMSE for the change in linear predictors for each coefficient is less than

eps. Default is1e-4.- max_iter

Maximum number of iterations (total across entire path). Default is 10000.

- dfmax

Maximum number of non-zero coefficients that may enter the model. Default is NULL (no maximum)

- warn

Return warning messages for failures to converge and model saturation? Default is TRUE.

- trace

If set to TRUE, inform the user of progress by announcing the beginning of each step of the modeling process. Default is FALSE.

- save_rds

Optional: if a filepath and name without the

.rdssuffix is specified (e.g.,save_rds = "~/dir/my_results"), then the model results are saved to the provided location (e.g., "~/dir/my_results.rds"). Accompanying the RDS file is a log file for documentation, e.g., "~/dir/my_results.log". Defaults to NULL, which does not save any RDS or log files.- return_fit

Optional: a logical value indicating whether the fitted model should be returned as a

plmmobject in the current (assumed interactive) session. Defaults to TRUE.- ...

Additional optional arguments to

plmm_checks()

Value

A list which includes 18 items:

beta_vals: The matrix of estimated coefficients. Rows are predictors (with the first row being the intercept), and columns are values oflambda.std_Xbeta: A matrix of the linear predictors on the scale of the standardized design matrix. Rows are predictors, columns are values oflambda. Note:std_Xbetawill not include rows for the intercept or for constant features.std_X_details: A list with 9 items:center: The center values used to center the columns of the design matrixscale: The scaling values used to scale the columns of the design matrixns: An integer vector of the nonsingular columns of the original dataunpen: An integer vector of indices of the unpenalized features, if any were specified in the designunpen_colnames: A character vector of the column names of any unpenalized features.X_colnames: A character vector with the column names of all features in the original design matrixX_rownames: A character vector with the row names of all features in the original design matrix; if none were provided, these are named 'row1', 'row2', etc.std_X_colnames: A subset ofX_colnamesrepresenting only nonsingular columns (i.e., the columns indexed byns)std_X_rownames: A subset ofX_rownamesrepresenting rows that passed QC filtering & and are represented in both the genotype and phenotype data sets (this only applies to PLINK data)

std_X: If design matrix is filebacked, the descriptor for the filebacked data is returned usingbigmemory::describe(). If the the data were stored in-memory, nothing is returned (std_Xis NULL).y: The outcome vector used in model fitting.p: The total number of columns in the design matrix (including any singular columns, excluding the intercept).plink_flag: Logical - did the data come from PLINK files?lambda: A numeric vector of the tuning parameter values used in model fitting.eta: A double between 0 and 1 representing the estimated proportion of the variance in the outcome attributable to population/correlation structure.penalty: A character string indicating the penalty with which the model was fit (e.g., 'MCP')gamma: A numeric value indicating the tuning parameter used for the SCAD or MCP penalties. Not relevant for lasso models.alpha: A numeric value indicating the elastic net tuning parameter.loss: A vector with the numeric values of the loss at each value oflambda(calculated on the ~rotated~ scale)penalty_factor: A vector of indicators corresponding to each predictor, where 1 = predictor was penalized.ns_idx: An integer vector with the indices of predictors which were non-singular features (i.e., features which had variation), where feature 1 is the intercept.iter: An integer vector with the number of iterations needed in model fitting for each value oflambdaconverged: A vector of logical values indicating whether the model fitting converged at each value oflambdaK: a list with 2 elements,sandU—s: a vector of the non-zero eigenvalues of the relatedness matrix K (note: K is the kinship matrix for genetic/genomic data; see the article on notation for details)U: a matrix of the eigenvectors of K associated withs

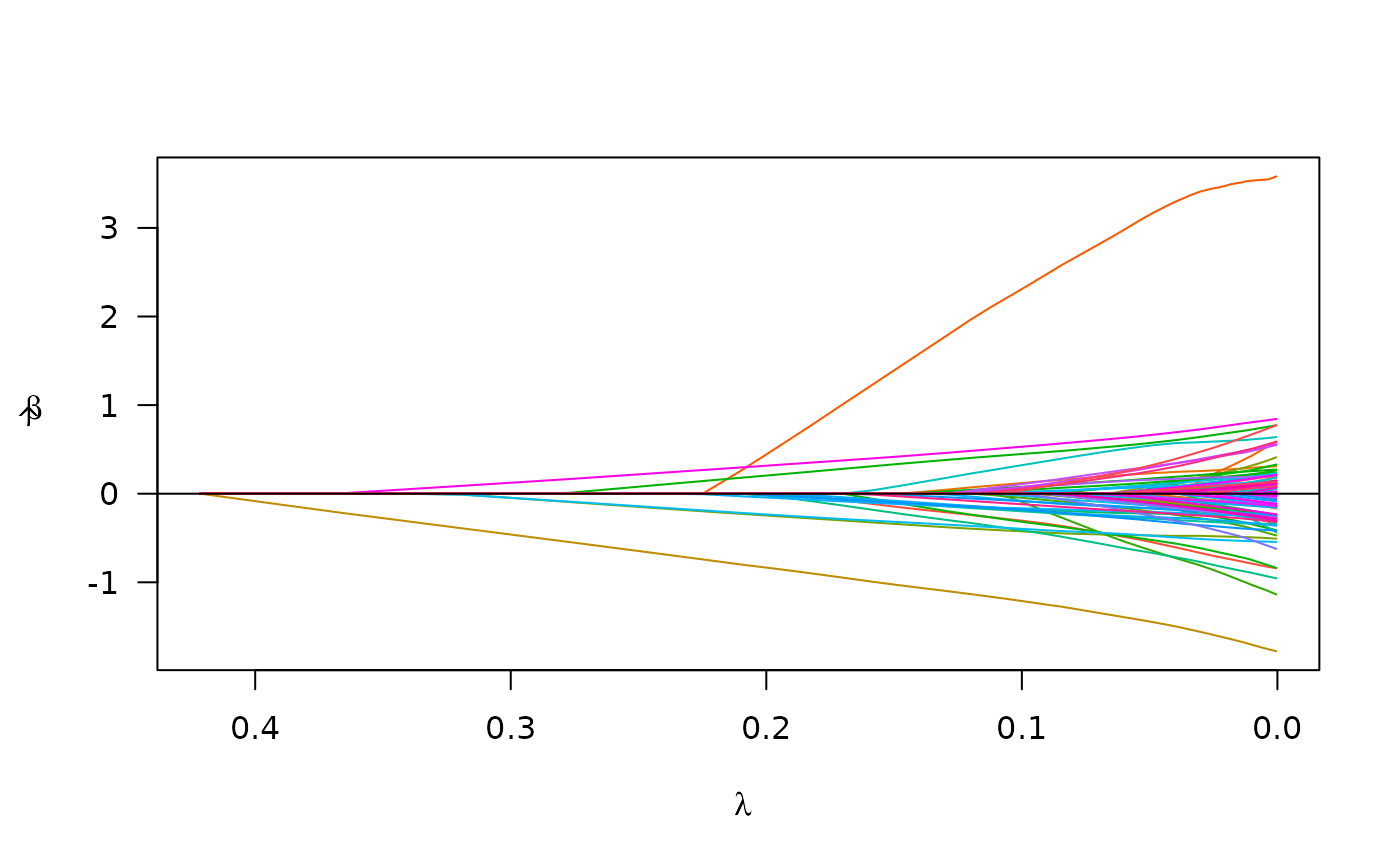

Examples

# using admix data

fit <- plmm(admix$X, admix$y)

s <- summary(fit, idx = 50)

print(s)

#> lasso-penalized regression model with n=197, p=101 at lambda=0.01404

#> -------------------------------------------------

#> The model converged

#> -------------------------------------------------

#> # of non-zero coefficients: 89

#> -------------------------------------------------

plot(fit)